Results from the 35th edition of The CMO Survey paint a challenging portrait of opportunity and challenges for marketing leaders. These findings arrive at a moment of notable economic stress, and the results reflect it — not just in the macroeconomic data, but in the patterns of behavior, investment, and strategic choices that run throughout the survey.

These results are based on survey responses from 308 marketing leaders at for-profit U.S. companies, 97% of whom hold positions at VP-level or above. Six key findings stand out.

Economic pessimism is at its highest point since the pandemic — and it is reshaping marketing priorities.

More than half of respondents report they are less optimistic than last quarter, with economic pessimism at its highest level since height of the pandemic in June 2020. This negative outlook and its triggers are reshaping marketing priorities. Tariffs are translating into price increases, with nearly half of companies raising or planning to raise prices this year. Among companies changing business investment levels, those signaling cuts outnumber those signaling increases by almost four to one. In response to this uncertainty, almost half of marketers are pulling back their targeting strategies to focus on increasing the loyalty of their existing customers rather than pursuing new customers, especially new geographic markets. Growth spending is following a similar pattern with companies spending almost 60% of their budgets on market penetration strategies that focus on selling more of existing products and services to existing customers. This inward orientation is a consistent theme across the 2026 findings.

AI is accelerating and delivering — but adoption is outpacing organizational readiness.

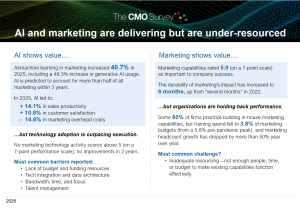

AI use in marketing has more than tripled since 2022, with generative AI growing especially fast. Companies project AI will account for more than half of all marketing activities within three years. And the business case is strengthening: measurable improvements in sales productivity, customer satisfaction, and marketing overhead costs have all risen year over year. Digital marketing’s contribution to company performance has also improved meaningfully, with nearly three quarters of companies rating its impact as strong. At the same time, we see evidence that technology adoption is outpacing organizational readiness. No marketing technology activity scores above 5 on a 7-point performance scale. This includes key steps such as “integrating marketing technologies into our customer funnel” and “generating ROI from marketing technologies.” The barriers are decidedly organizational — factors such as budget, integration, bandwidth, and talent dominate. Companies will need to ensure that their investments in technology are matched with investments in the capabilities needed to use it effectively.

Marketing capabilities are viewed as critical — yet companies are underinvesting in the people needed to develop them.

Marketing capabilities are rated as important to business success — averaging 5.9 on a 7-point scale — and companies overwhelmingly rely on building them through training and hiring as their primary approach. Yet training budgets have fallen steadily for years, now standing at just 3.8% of marketing spending, down from a pre-pandemic high of 5.8%, and marketing headcount growth has slowed sharply, declining more than 50% from last year’s rate. It is not surprising then that the most cited capability gap is not a missing skill, but inadequate resourcing — not enough people, time, or budget to make existing capabilities function effectively.

Marketing’s mandate is expanding, but organizational support is not keeping pace.

Marketing’s formal responsibilities have grown significantly since 2025, with notable increases in managing revenue growth, public relations, and customer insight. Marketing leaders are also participating more frequently in board meetings. Yet the CMO-CFO partnership has barely moved in four years — rated just 4.5 on a 7-point scale for building a business case for marketing spending and fewer than half of companies report marketing and finance work together on growth. Marketers devote roughly twice as much time managing the present (68%) as preparing for the future (32%) every year since 2019. Pressure from CEOs, boards, and CFOs is reinforcing that short-term orientation. The predominant response to this pressure from marketing leaders is a shift toward short-term impact over long-run gains (70.6%) and a return to established strategies (47.1%). Rather than investing in deeper customer insights, most marketers focus on developing stronger performance tracking as the primary way to demonstrate value.

Marketing spending decisions remain more reactive than strategic — shaped more by financial pressure and executive reflex than by marketing priorities.

Marketing budgets have fallen to their lowest share of company revenues and budgets in several years — 9.0% of revenues and 9.6% of overall budgets — and overall marketing spending grew just 1.7% over the prior 12 months, the smallest rate increase since 2021. When profits fall short of expectations, 53.1% of company executives focus on cutting expenses rather than investing in revenue growth — up from 46% one year ago. When this occurs, marketing expenses are cut 45.4% of time — more frequently than other expense categories. This challenges other survey findings that show the durability of marketing’s impact on customers has grown meaningfully since 2022 — increasing up to six months in duration. In another contradiction, although almost half of marketers cite building loyalty and retention among existing customers as their primary strategic response to economic uncertainty, acquisition spending is now 26% larger than retention spending and growing — even as customer retention is outperforming acquisition in the performance data.

Channel findings point in a more expansive direction.

Channel strategies are expanding meaningfully, with 57.6% of companies increasing the number of channels they use and digital and physical channel growth occurring in parallel rather than as substitutes. Companies are adding digital channels (47.9%), social selling (38.8%), new face-to-face channels (30.3%), and retail media (23.6%). This broad-based expansion stands in contrast to the inward orientation visible in other parts of the survey and suggests that marketers see the customer interface as a place worth investing even in a cautious environment.

Three reports, which are provided free of charge at cmosurvey.org, summarize these and other results from the 35th edition. The Highlights and Insights Report shares key survey metrics, trends, and insights over time, The Topline Report offers an aggregate view of survey results, and The Firm and Industry Breakout Report examines results by company sector, headcount, and sales.https://cmosurvey.org/results/